Superannuation budget measures one step closer

December 1, 2021Several superannuation proposals announced in this year’s Federal Budget have been introduced into Parliament in the Treasury Laws Amendment (Enhancing Superannuation Outcomes for Australians and Helping Australian Businesses Invest) Bill 2021.

These measures – all due to start on 1 July 2022 – aim to:

- improve flexibility for Australians preparing for retirement

- reduce costs and simplify reporting for SMSFs

- expand the superannuation guarantee (SG) to lower income earning individuals, and

- support more Australians to own their first home.

- The superannuation measures that have been introduced include:

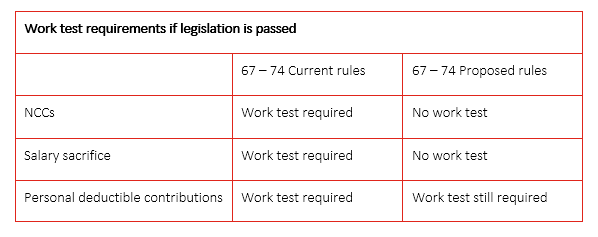

Repealing the work test for individuals aged 67 to 74

Start date: 1 July 2022

Individuals aged 67 to 74 will be able to make or receive non-concessional contributions (NCC) or salary sacrifice superannuation contributions without meeting the work test, subject to existing contribution caps.

However, individuals aged 67 to 74 years wanting to make personal deductible contributions will still have to meet the existing work test.

Removing the work test for individuals aged 67 to 74 will provide more flexibility for retirees under 75 to top up their superannuation without needing to work 40 hours within 30 consecutive days in a year prior to making a contribution. It will also allow advisers to implement strategies, such as the re-contribution strategy, that are not normally available to retired clients in this age group.

The table below summarises the key changes.

Note – the removal of the work test will not enable individuals approaching age 75 to access the bring forward rule for years in which they have no cap space. This is because under current legislation, individuals are not able to make voluntary superannuation contributions beyond the age of 74, so allowing an individual who is aged 74 to bring forward two years’ worth of NCC contributions would enable them to access a contribution period for which they are not entitled to.

Reducing the eligibility age for downsizer contributions to 60

Start date: 1 July 2022

The eligibility age to make a downsizer contribution will be reduced from 65 to 60 years of age. All other eligibility criteria that currently apply to downsizer contributions will continue to apply.

To recap, the downsizer contribution rules allow individuals to make a one-off after-tax contribution to superannuation of up to $300,000 (or $600,000 per couple) from the proceeds of selling their home they have held for at least 10 years. Under the rules, both members of a couple can make downsizer contributions for the same home and the contributions do not count towards an individual’s NCC cap.

Reducing the eligibility age for downsizer contributions to age 60 could allow an eligible couple in their early sixties to sell their home and contribute up to $1,260,000 to superannuation in a year by each making a downsizer contribution of $300,000 and NCCs of $330,000.

Providing SMSFs choice to calculate exempt current pension income

Start date: 1 July 2022

SMSF trustees will be able to choose how to calculate exempt current pension income (ECPI) where the fund is fully in the retirement phase for part of the income year but not for the entire income year.

In other words, choice applies where a SMSF has member interests in both accumulation and retirement phases at one time, but only retirement phase interests at another time in an income year.

Currently, the ATO holds the view that the assets of the fund will be segregated during this period (ie, when the fund is fully in retirement phase) meaning the fund may need to use both the segregated and proportionate methods for calculating ECPI for the one year.

This change will allow trustees to choose to apply the proportionate (or unsegregated) method for the whole of the income year based on a single actuary’s certificate, rather than being required to use different methods to calculate ECPI for different periods in the same income year.

However, the choice only applies if the SMSF does not have disregarded small fund assets (DSFA).

To recap, an SMSF is regarded as having DSFA where the fund:

- pays a retirement phase pension at any time during the financial year, and

- a fund member has a total superannuation balance of $1.6 million or more on 30 June of the previous financial year, and

- the same member is receiving a retirement pension from any fund (not necessarily the SMSF).

Points to note about making a choice:

- Trustees will be able to choose which method to use and calculate ECPI before submitting the fund’s SMSF annual return.

- This choice is not a formal election and does not have to be submitted to the ATO. However, it is expected that trustees will keep a record of any choice they make and the details of the calculation they use.

- If the trustee does not make a choice, then the fund’s ECPI will be calculated using the segregated method for any period of the income year where all of the interests in the fund are in retirement phase for some, but not all, of the income year.

To summarise, an SMSF will only be able to exercise this choice if:

- all of the interests in the SMSF are in retirement phase for some, but not all, of the income year, and

- all of the income derived from the SMSF’s assets is supporting retirement phase income stream benefits payable from an allocated pension, market linked pension or an account-based pension, and

- the SMSF does not have DSFA.

Removing the $450 per month minimum SG threshold

Start date: 1 July 2022

The $450 per month minimum SG income threshold will be repealed. As a result, employers will be required to make quarterly SG contributions on behalf of low-income employees earning less than $450 per month (unless another SG exemption applies).

Under the current rules, an employer is not required to pay SG contributions for an employee who earns less than $450 per month.

The two main rationales for the $450 threshold were to:

- Minimise the administrative burden on employers administering small amounts of superannuation contributions. However, technological advances and the digitalisation of payroll systems, for example Single Touch Payroll, diminishes the rationale for a minimal threshold which adversely impacts low-income workers and women.

- Prevent the creation of low-balance accounts that could get eroded by fees and insurance premiums. However, recent Government changes have reduced the impact of these risks.

This measure will benefit an estimated 300,000 people or 3% of employees[1]. These people are mainly young and/or lower-income and part-time workers, and around 63% are female[2]. These changes will help these workers to start accumulating superannuation earlier as well as help address the gap in superannuation savings between women and men.

Increasing the first home super saver scheme (FHSSS) releasable amount to $50,000

Start date: 1 July 2022

Since 1 July 2017, individuals can make voluntary concessional contributions (CC) and NCCs into superannuation and have them released to help pay for their first home.

The maximum releasable amount of eligible voluntary CCs and NCCs under the FHSSS will be increased from $30,000 to $50,000.

Under the new rules, the maximum amount of voluntary contributions that are eligible to be released remains at $15,000 per financial year and $50,000 in total. The individual will also receive an amount of earnings that relate to those contributions.

Therefore, an individual would need to contribute over four years to take maximum advantage of the scheme under this measure.

This information has been prepared without taking into account your objectives, financial situation, or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation or needs. Content in partnership with Taxpayers Australia