Personal services income explained

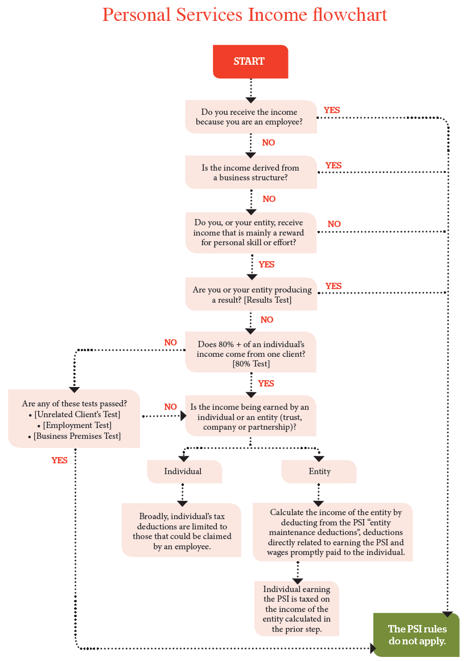

December 3, 2019The personal services income (PSI) rules apply to income that is earned mainly from the personal efforts or skills of a person.It does not matter whether the income is earned by the individual in their own name or through an entity such as a business. The rules do not apply to income earned from being an employee.

A business structure

This can be a confusing concept. It does not mean that you conduct a business through an entity such as a company or a trust.

The term “business structure” is used to define a business (operated through any structure) that is large enough for it to be concluded that the income of the business is not being earned from the individuals in the business. Rather, the income is being earned by the “business structure”. This can still apply to quite small businesses.

The tests

The results test

This is an important test. If you pass the test, the PSI rules do not apply to you. An individual passes the results test if in relation to at least 75% of the individual’s PSI:

- it is for producing a result, and

- the individual is required to supply the equipment or tools of trade needed to perform the work, and

- the individual is liable for rectifying any defect in the work.

Unrelated clients test

This test is passed if:

- the PSI is gained from providing services to two or more entities that are not associates, and

- the work has been gained by making invitations to the public or a section of the public.

Employment test

Broadly, this test is passed if:

- one or more entities are engaged (other than associates) to perform work, and

- those entities perform at least 20% by market value of the principal work. The test is also passed if an apprentice is engaged for at least half the income year.

Business premises test

Broadly, this test is passed if business premises are maintained:

- at which the PSI is mainly gained, and

- of which there is exclusive use, and

- that are physically separate from premises the individual or associate uses for private purposes, and

- are physically separate from premises of customers or associates of customers.

Personal services determination

The ATO can give you a ruling that the PSI rules don’t apply to you in certain circumstances. For example, there could be “one-off” changes in your circumstances that cause you to fail the PSI tests. You can apply to the ATO to have the PSI rules ignored by the ATO. If the ATO rules in your favour, this is called a “personal services determination”.

This information has been prepared without taking into account your objectives, financial situation, or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation or needs. Content in partnership with Taxpayers Australia.